We Do Curated, High-Probability Stock Pairs for Pairs Trading – Powered by Our Advanced Signals Service

Looking for reliable stock pairs trading opportunities in the US stock market? Our carefully curated service delivers near-real-time trading signals from 60–100 of the strongest cointegrated and correlated US stock & ETF pairs ready for trading at any time. We help experienced retail traders capture statistical arbitrage profits with confidence.

We continuously refine our stock pair universe through rigorous quarterly re-screening and backtesting. This dynamic process ensures we keep only the highest-quality pairs, add promising new ones, and remove those that no longer meet our strict criteria — striving to deliver you a tradeable edge in ever-changing markets.

Our High-Quality Securities Universe & Quarterly Backtest Framework

We start with a robust foundation designed for liquidity, tradability, and fundamental alignment:

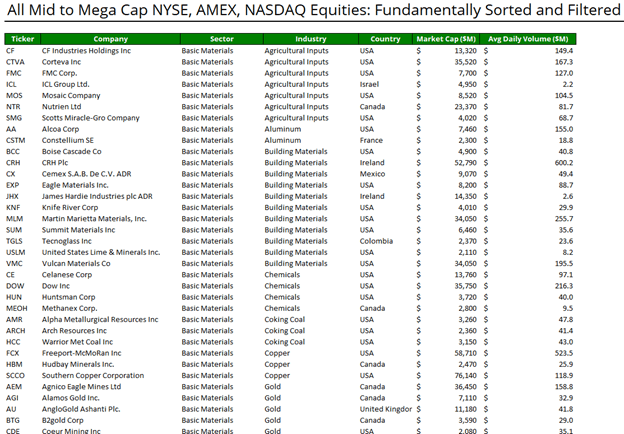

- US-listed stocks & ETFs only (NYSE, NASDAQ, AMEX)

- Market cap > $2 billion, or $500m+ for ETFs

- Average daily volume >$2 million minimum, median >$60m

- Easy-to-borrow for short selling

- Fundamentally correlated: same national market + same sector (usually same industry sub-group; adjacent sub-sectors occasionally included)

- Strong preference for pairs with similar beta and market capitalization

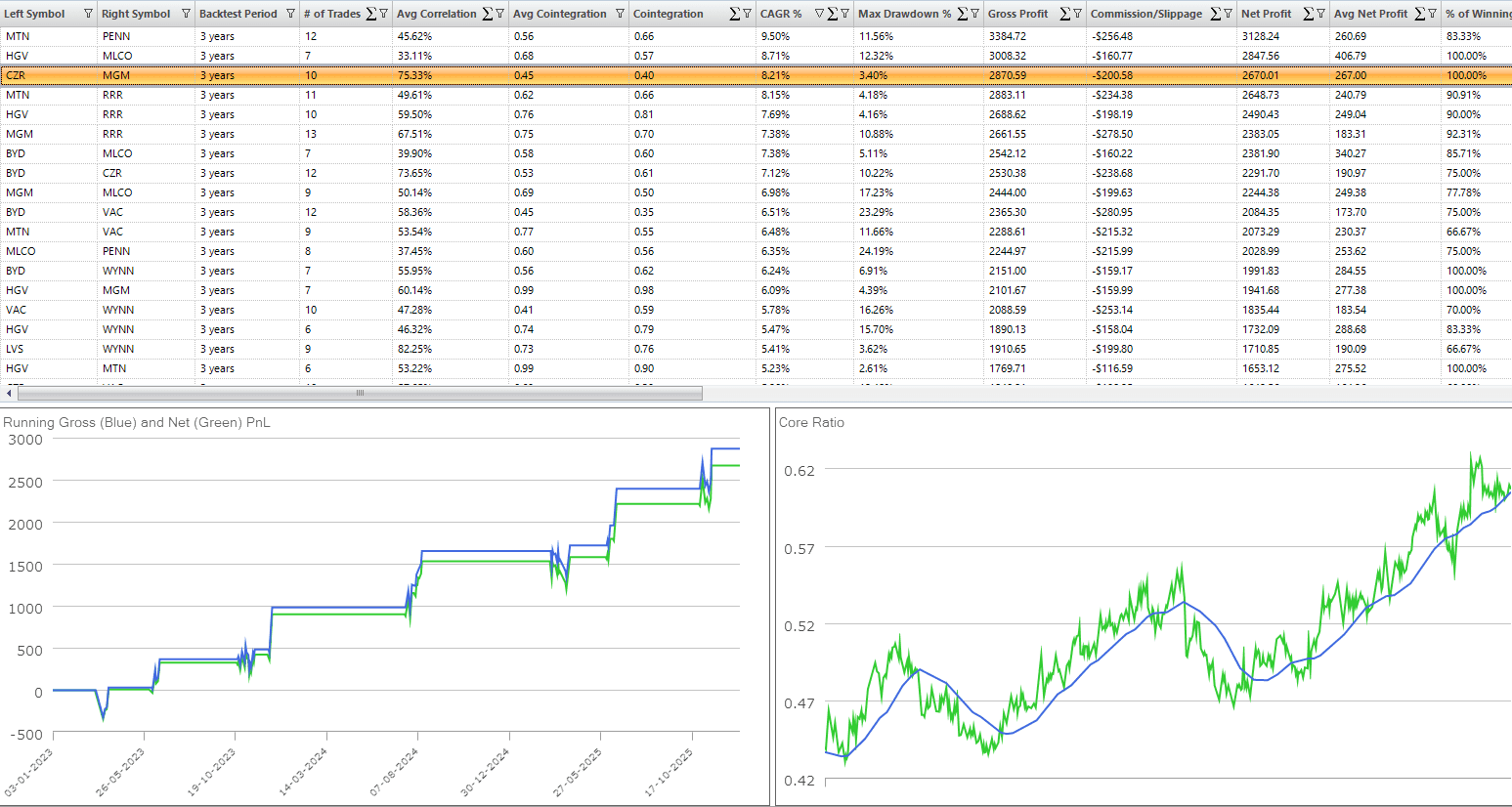

Backtesting & Signal Generation Parameters

Our signals are built on proven mean-reversion logic, tested over a 3-year lookback period:

- Price Ratio uses 60-day standard deviation and simple moving average lookback settings

- Dual-layer entry system for enhanced risk control:

- Layer 1: Enter at ±2.5 standard deviations from the mean ($3,000 per leg)

- Layer 2: Add at ±3.5 standard deviations ($3,000 per leg)

- Both layers exit simultaneously at ±1.0 standard deviation on the moving average of the core ratio

- ETFs traded at Layer 1:±2.0 standard deviations and Layer 2: ±3.0 sd, Exit at ±0.5 sd

- Position sizing based on a hypothetical $100,000 account and 3% of account equity ($3,000) per leg

- We strongly recommend starting with paper trading or significantly smaller leg sizes while learning the system

- Realistic 0.10% commissions + slippage per trade (based on Interactive Brokers’ average execution costs)

- Strict time stop of 50 maximum days in trade

Rigorous Filters for the Highest-Probability Pairs

We apply multiple performance filters to select only the best candidates each quarter:

- Cointegration — Tested via the Augmented Dickey-Fuller (ADF) test; we target p-values of 0.10 or lower (strong evidence of mean reversion)

- Correlation — Aim for 50%+; lower values accepted only for exceptionally strong cointegration and top scores on other metrics

- Average profit per trade — Minimum $120, with $150+ preferred (dual-layer trades count as one)

- Trade frequency — At least 5 trades over the 3-year backtest

- Risk-adjusted performance — CAGR% of net profits preferably exceeds maximum drawdown (positive reward/risk on a self-financing basis)

- Maximum drawdown targeted < 20%, ideally < 15%

- Win rate — Minimum 70%, targeting >80%

- Commissions/slippage impact — Must remain < 20% of gross profit

- Volatility: keep measured pair Ratio volatility within acceptable limits

Wild Card Pairs – High-Potential Exceptions

We occasionally include Wild Card pairs that miss our standard correlation or cointegration thresholds but show outstanding in-sample backtest results over the past three years. These deserve close monitoring — and often become tomorrow’s top performers.

Ready to trade smarter with high-probability pairs trading signals?

Explore our service today and let us do the heavy lifting for you!

Important Risk Disclosure

These stock pair examples and performance metrics are provided for informational and educational purposes only. They are not personalized investment advice. Past performance — including simulated results from our White Paper Silverfire Beta account (via Interactive Brokers’ paper trading) — does not guarantee future results. Trading pairs using our signals involves substantial risk of loss. Actual results will vary due to market conditions, execution, slippage, and other factors. Please review our full Risk Disclosure before trading.

Prior Testimonials (from our 2009-2011 service)

Frequently Asked Questions

Still have questions? We’ve got answers!

In a world flooded with generic trading signals that chase trends, deliver directional bets, and rarely beat passive indices after fees and risk—most services fail spectacularly.

The 2024–2025 SPIVA data confirms it: 80–94% of active managers underperform benchmarks over long horizons, even on risk-adjusted terms.

Silverfire Research is different—and as far as available evidence shows in early 2026, we're the only provider delivering near-real-time US stock pair trading signals directly to a private Discord channel.

We harness the same powerful equity statistical arbitrage strategy employed by top hedge funds: market-neutral long/short pairs that exploit temporary price divergences in cointegrated stocks, reducing directional market risk dramatically.

Our Silverfire Beta White Paper proves the edge with transparent, simulated results in an Interactive Brokers account:

- 432 trades over 7.5 months

- +17.4% return (+28.8% annualized)

- Max drawdown: just -3.6%

- Sharpe ratio: 1.7

- Sortino ratio: 3.8

This crushed the S&P 500 (+10.8%) and First Trust Long/Short Equity ETF (+3.8%) over the same period—with far lower volatility and drawdown.

Powered by the industry-leading PairTrade Finder® platform (founded 2008, trusted by professionals), our signals arrive 2–3 times per day during US sessions, high-probability setups ready for easy implementation by sophisticated self-directed traders.

No hype, no AI-generated noise, no "2 and 20" hedge fund fees—just rigorous, backtested, market-neutral edge at $99/month.

If you're tired of underperforming signals and ready for verifiable low-risk outperformance, subscribe now.

Download the White Paper first—see the proof yourself.

Trading involves risk; past performance isn't indicative of future results, but our mission is simple: deliver what actually works.

We are focusing on a niche in the trading services industry, providing a service that we strive consistently to ensure actually works. We seek to deliver to sophisticated self-directed traders and investors a easy-to-implement trading strategy that can produce higher risk-adjusted returns that passive equity index investing.

If you read our Silverfire Beta White Paper, available above, and you focus on Slide 3 "The Power of Equity Statistical Arbitrage", one might reasonably assume that a self-directed equity stat arb trader with a decent system may reach a Sharpe ratio of 2 or more, as they will avoid the typical "2 and 20" fee structure paid by hedge fund investors.

Additionally, by applying greater leverage than insitutional hedge funds to the strategy (provided risk management is maintained), they might reasonably be expected to match or exceed the long-term S&P 500 return but with a far lower risk profile. Our mission is to see whether our service can allow traders to achieve this outcome. Our 2025 beta test easily did so.

The majority of stock trading signals services and newsletters underperform the indices on a risk-adjusted basis and have no particular value e.g. the 2024 SPIVA scorecard revealed that 94% of active domestic equity funds underperformed the S&P Composite 1500 over 20 years, with underperformance rates remaining high (around 80-90%) even on a risk-adjusted basis across various horizons and asset classes. Additionally, a 2024 investigation into news sentiment-based signals (using data from 2010-2020) concluded that such indicators have limited predictive power and fail to generate consistent risk-adjusted outperformance over indices, with sentiment-driven strategies yielding negative Sharpe ratios and underperforming passive buy-and-hold approaches after transaction costs.

Silverfire Research LLC is solely dedicated to analysing and producing the highest-probability stock pair trading signals it is able. We believe there are 100's of potential US stock pair trading opportunities every single day - we look to provide you with 40-60 of the best of them every month. That is our mission, and we are focused.

Members of our group may and do pair trade stocks using our system and methodology on a regular basis. However, these activities are outside of, and unrelated, to Silverfire Research LLC.

Our general win rate is between 65% - 75% with the avg. win being slightly smaller than the avg loss. Please go to Our Performance page to see the latest results.

Our service is priced at $95/month for personal retail use because we deliberately target sophisticated self-directed traders who seek genuine edge without the exorbitant costs of traditional alternatives.

The vast majority of stock trading signals services and newsletters fail to deliver value, consistently underperforming passive indices on a risk-adjusted basis.

The 2024 SPIVA U.S. Scorecard shows that over 20 years (through December 2024), around 92-94% of domestic equity funds underperformed benchmarks like the S&P Composite 1500, with even higher rates (often 90%+) on risk-adjusted metrics across horizons.

In contrast, hedge funds offering equity statistical arbitrage strategies typically charge "2 and 20" fees—2% management plus 20% of profits—eroding returns significantly for investors.

Our mission focuses on a niche: delivering an easy-to-implement, evidence-based equity stat arb strategy that our 2025 beta testing showed can achieve high Sharpe ratios (potentially 2+), enabling retail traders to match or exceed long-term S&P 500 returns with lower risk through careful leverage—without those heavy fees.

By keeping pricing accessible at $95/month, we prioritize accessibility and real results over profit maximization, unlike most services that charge premium rates yet provide little edge.

This structure aligns incentives with yours: sustainable outperformance, not hidden costs.

Silverfire Research LLC is headed by former investment banker, family-office executive, hedge fund manager and current professional trader, Geoff S.T. Hossie, CMT. Geoff and his team of programmers have been in this business for a long time, over 56 years combined. Geoff’s CV is available here.

We use stock pair trading, also known as market neutral, long/short equity trading, statistical arbitrage or relative value trading. It is a strategy that has stood the test of time (see white paper on equity stat arb fund returns 2021-2025).

Sign up above and receive our White Paper that explains our equities pair trading strategy in detail, with an example pair analysis, and tracks our beta portfolio's simulated trading performance over 432 closed trades in 7.5 months.

A detailed description of our pair selection criteria and trading parameters applied can be found here.

Most stock trading signals services and newsletters fail to deliver consistent value, with the majority underperforming passive indices on a risk-adjusted basis.

The latest SPIVA® U.S. Mid-Year 2025 report shows that 54% of large-cap U.S. equity funds underperformed the S&P 500 in the first half of 2025 (an improvement from 65% in 2024), but longer-term data remains stark: over 15 years through 2024, no major equity category saw a majority of active managers outperform their benchmarks, with underperformance rates often exceeding 80-90% in many segments.

In contrast, Silverfire Research stands out by focusing exclusively on a proven, market-neutral equity statistical arbitrage strategy: high-probability stock pair trading.

We deliver near-real-time signals directly to a private, subscription-only Discord channel, powered by the industry-leading PairTrade Finder® software platform (founded in 2008, with thousands of downloads and used by professionals worldwide).

Our edge comes from rigorous, transparent performance:

- The Silverfire Beta White Paper documents 432 trades over 7.5 months in a simulated Interactive Brokers account, achieving +17.4% return (+28.8% annualized), with a max drawdown of just -3.6%, Sharpe ratio of 1.7, and Sortino ratio of 3.8.

- This significantly outperformed the S&P 500 (+10.8%) and the First Trust Long/Short Equity ETF (+3.8%) over the same period, with far lower risk.

Backed by a team with over 56 years of combined experience in discretionary/algorithmic trading, investment banking, system engineering, and software development—and direct ties to PairTrade Finder®'s founders—we prioritize evidence-based, easy-to-implement signals over hype.

Unlike generic signals providers (often AI-driven, sentiment-based, or directional) that rarely publish verifiable long-term results and frequently chase trends with higher volatility, Silverfire offers:

- Market-neutral exposure (long/short pairs reduce directional beta).

- High-probability setups rooted in statistical relationships.

- Professional-grade tools without the "2 and 20" hedge fund fees.

For sophisticated self-directed traders seeking real edge with controlled risk, we deliver what most competitors promise but rarely achieve: verifiable, low-drawdown outperformance.

Download our White Paper to see the proof.

We understand that trust is essential when considering any trading signals service, especially in a field where many offerings fall short of expectations.

Silverfire Research operates as Silverfire Research LLC, a registered company based in the United States (address: 30 N Gould Street, Suite R, Sheridan, WY 82801 U.S.A.), and we are fully committed to complying with all applicable U.S. laws and regulations.

Our service is strictly for personal, non-professional use by sophisticated self-directed retail traders. Subscriptions are handled securely through Stripe, a leading payment processor—we never access, store, or view your financial or payment information, as it remains protected within Stripe's secure environment.

Importantly, there is no binding contract upon signup: you can cancel at any time, and access is provided on a month-to-month basis via a private Discord channel.

Trading involves substantial risk of loss and is not suitable for everyone. Past performance, including our published beta results, is not indicative of future results.

We strongly recommend reviewing our full disclaimers, terms of service, and the Silverfire Beta White Paper (available on the site) before subscribing—these clearly outline that signals are for informational purposes only, not personalized advice, and you trade at your own risk.

Our team, led by Geoff S.T. Hossie, CMT (Chartered Market Technician bound by the CMT Association’s Code of Ethics), brings over 56 years of combined experience in trading, investment banking, and software development.

We focus on transparent, evidence-based pair trading signals powered by the established PairTrade Finder® platform.

We encourage you to download our White Paper, examine the verifiable simulated track record, and decide if our market-neutral approach aligns with your goals.

As with any investment service, conduct your own due diligence.